The story so far

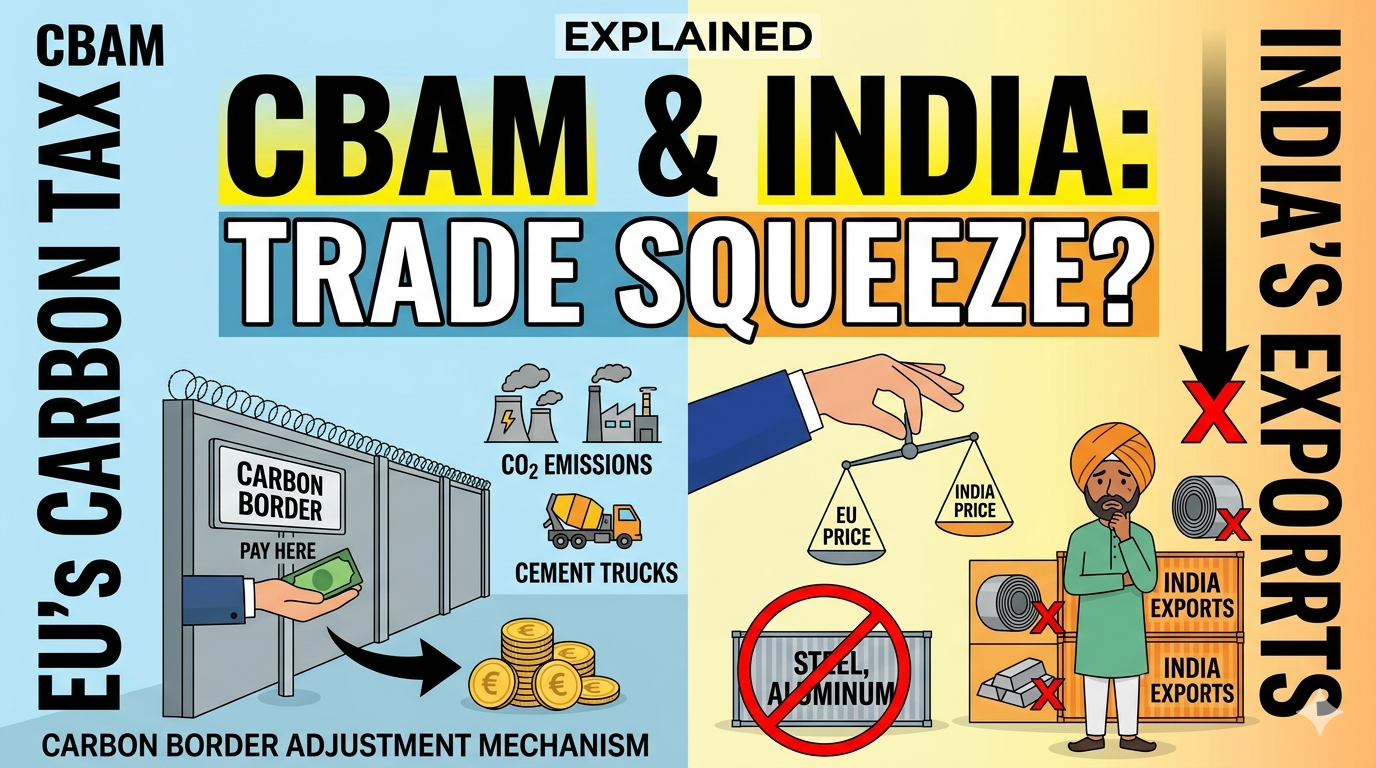

In January 2026, the European Union switched on the payment phase of its Carbon Border Adjustment Mechanism, or CBAM. For the first time in history, a major economy is putting a price on the carbon embedded in goods crossing its borders — not on the carbon released inside its own factories.

On June 1, 2026, a peer-reviewed study by the Potsdam Institute for Climate Impact Research (PIK), published in the Journal of the Association of Environmental and Resource Economists, made a striking claim. According to the study, CBAM could increase global emission reductions by 73 per cent compared with what the EU's domestic climate policy can achieve on its own — provided countries like Canada, Japan, South Korea and Taiwan respond with their own carbon pricing systems.

For Indian exporters of steel, aluminium and cement, however, CBAM is not an academic question. It is already showing up in shrinking order books and tighter margins.

This explainer walks through the five Ws: what CBAM is, why the EU introduced it, when and where it applies, who is affected, and what the way forward looks like for India.

What is CBAM, in simple words?

CBAM stands for Carbon Border Adjustment Mechanism. Think of it as a carbon-price tag stuck on imports.

Inside the EU, factories already pay a carbon price under a system called the EU Emissions Trading System (EU ETS). They must buy permits for every tonne of CO₂ they release. This makes EU-made goods more expensive than goods made in countries where carbon is essentially free to emit.

CBAM fixes that gap at the border. If a country exports steel, cement, aluminium, fertiliser, hydrogen or electricity to the EU, and that country does not already have a comparable carbon price, the EU charges an equivalent levy at the border. In effect, the importer must buy "CBAM certificates" that match the carbon emissions embedded in the imported product.

The carbon price applied is linked to the EU ETS price, which has historically hovered around the €70–€90 per tonne range (this fluctuates, and readers should verify the current price before quoting it).

Why has the EU introduced CBAM?

The EU points to one core problem: carbon leakage.

Carbon leakage happens when strict climate rules in one region simply push polluting production to another region. A European steel plant facing a high carbon price could shut down and shift production to a country with no carbon price. Global emissions do not fall — they just move addresses. Worse, the EU loses both the factory and the climate benefit.

The Potsdam study quantifies this neatly. According to the study's modelling, a European carbon price of about $100 per tonne would cut EU emissions by roughly 505 million tonnes of CO₂ a year. But around 40 per cent of that cut would be cancelled out by emissions rising elsewhere — as production migrates and global fossil-fuel prices soften. The net climate gain is only about 305 million tonnes.

With CBAM in place, the study estimates carbon leakage falls from 40 per cent to 15 per cent. Global emission reductions rise to about 399 million tonnes a year. And if major trading partners introduce their own carbon prices in response, the figure climbs further to 691 million tonnes a year — the 73 per cent boost the study highlights.

A short word of caution: these figures come from one specific economic model using trade data across 56 sectors and 43 countries. They are projections, not measured outcomes. Other studies, as we'll see below, reach more sceptical conclusions.

When did CBAM come into force?

CBAM was rolled out in two phases.

The transitional phase ran from October 2023 to December 2025. During this period, EU importers only had to report the emissions embedded in their imports. No money changed hands.

The definitive phase began on January 1, 2026. From this date, importers must actually buy CBAM certificates to match the embedded emissions of their goods. The financial bite is now real.

The EU has also signalled that CBAM coverage will expand. Reports suggest that around 180 additional steel- and aluminium-based downstream products could be added from January 1, 2028, though aspirants should verify this against the official EU notification before quoting it as fact.

Where does CBAM apply? Which sectors are covered?

Right now, CBAM covers six categories of goods:

- Iron and steel

- Aluminium

- Cement

- Fertilisers

- Electricity

- Hydrogen

These are described as emissions-intensive trade-exposed (EITE) sectors — industries where production is heavily polluting and deeply linked to international trade. Together, they account for a large share of industrial CO₂ emissions.

The Potsdam study and other policy papers suggest CBAM may eventually extend to more sectors, including downstream products like steel pipes, aluminium foil, and certain chemicals. Wider sectoral coverage, according to the study, would significantly strengthen global climate cooperation.

Who is affected — and where does India stand?

Any country exporting CBAM-covered goods to the EU is affected. But the impact is uneven. Three countries are commonly described as the most exposed: India, China, and Türkiye.

For India, the numbers are sobering, though estimates vary widely by source:

- A 2024 study by the Centre for Science and Environment (CSE) reportedly found that CBAM-covered goods accounted for nearly 10 per cent of India's total exports to the EU in 2022–23 (this should be verified from the original CSE report).

- The same CSE analysis estimated that CBAM could impose a price burden of roughly 25 per cent on affected exports.

- The Global Trade Research Initiative (GTRI), in early 2026, estimated that Indian exporters of steel and aluminium may need to slash prices by 15–22 per cent just to retain EU market share.

- Industry data reported by AL Circle indicates Indian unwrought aluminium exports to the EU fell by approximately 41 per cent between year-to-date January 2025 and the same period in 2026 — although attributing the full drop to CBAM alone is difficult, since other market factors are at play.

- The CSEP (Centre for Social and Economic Progress) has noted that CBAM-targeted exports make up only about 0.2 per cent of India's GDP, suggesting the macroeconomic hit is modest even if specific sectors are bruised hard.

Indian steel is structurally more exposed than European steel because nearly half of India's production reportedly comes from coal-based blast furnaces, giving it a higher carbon footprint per tonne than the EU's electric-arc-furnace-heavy industry. Readers should verify the exact emissions-intensity figures from official sources such as the Ministry of Steel before citing them.

What is the "Brussels effect"?

This is where the Potsdam study connects to a bigger idea in international politics.

The "Brussels effect" is a term coined by legal scholar Anu Bradford of Columbia Law School around 2012. The argument, in plain English, is that the EU's huge consumer market gives it the power to set global rules — not by force, but simply because companies and countries find it cheaper to follow EU standards everywhere than to maintain two production lines.

We have seen this with the General Data Protection Regulation (GDPR) reshaping global data privacy practices, and with EU chemical and food-safety rules influencing manufacturing far beyond Europe.

The Potsdam Institute argues that CBAM could trigger a Brussels effect for climate policy. If exporting to the EU means paying a carbon levy at the border, countries may decide it is smarter to set up their own carbon pricing systems — keeping the revenue at home instead of handing it to Brussels. The study identifies Canada, Japan, South Korea and Taiwan as the most likely candidates to "join the climate coalition" in this way. The United States could follow if CBAM expands further. China, the study notes, would currently find participation economically attractive only if the carbon price stayed below $20 per tonne.

The study's authors are upfront that these are model-based estimates. The lead author, Timothé Beaufils, frames the finding as a "strong indication" rather than a prediction set in stone.

What are the problems with CBAM?

CBAM is not without serious criticism. Three main objections come up repeatedly:

One — it shifts costs to developing countries. Critics argue that CBAM forces poorer countries to pay for the EU's decarbonisation ambition while the EU itself faces no equivalent obligation to provide climate finance, technology transfer, or transition support. This sits awkwardly with the United Nations climate principle of Common But Differentiated Responsibilities (CBDR), which recognises that rich countries — having burned the most carbon historically — should shoulder more of the burden.

Two — its actual climate gains are uncertain. A 2024 report by the CSE, and a separate study by the African Climate Foundation, argue that CBAM's emission reduction impact will be limited in practice. Both reports point out that the levy raises money for the EU but provides no clear pathway for that revenue to finance industrial decarbonisation in the developing world.

Three — it raises trade-law questions. Whether CBAM is fully compatible with the World Trade Organization's non-discrimination rules remains contested. India has raised these concerns in international forums.

A fourth, more practical issue dominates conversations among Indian exporters: the data problem. CBAM requires plant-level emission data, third-party verified by EU-recognised auditors. For India's many small and medium steel and aluminium units, this is a heavy compliance burden. Where verified data is missing, EU authorities can apply default emission values — which are deliberately set on the high side, so unverified exporters pay more.

What is India doing about it?

India's response is moving on several tracks at once.

The Carbon Credit Trading Scheme (CCTS): Notified in June 2023 under the Energy Conservation (Amendment) Act, 2022, this is India's emerging domestic carbon market. As of April 2025, compliance obligations are reportedly in force for around 490 entities across seven energy-intensive sectors (aluminium, cement, chlor-alkali, pulp and paper, petroleum refining, petrochemicals, and textiles), administered by the Bureau of Energy Efficiency (BEE). The first Carbon Credit Certificate (CCC) trading is expected to launch by mid-to-late 2026. If India can demonstrate that a credible domestic carbon price has already been paid, Indian exporters may be able to claim deductions against CBAM liabilities at the EU border.

India Border Adjustment Mechanism (IBAM): There has been policy discussion around introducing an Indian equivalent of CBAM, sometimes referred to as IBAM, to retain carbon-related revenues within India rather than letting them flow to the EU's general budget. Whether and when this will be formally introduced is unclear, and readers should treat this as a proposal under examination rather than a notified policy.

India–EU Free Trade Agreement: The text of an India–EU FTA was reportedly finalised in early 2026, but does not exempt India from CBAM. The deal reportedly includes an annex providing procedural engagement and a most-favoured-nation clause, so any flexibility granted to other countries should extend to India. Aspirants should verify the latest official status of the FTA before quoting specific provisions.

Industrial decarbonisation push: Indian steel majors are being nudged toward greener production routes — electric arc furnaces, gas-based direct reduced iron, scrap-based recycling, and eventually green hydrogen. Government and private sector roadmaps for hard-to-abate sectors are being developed.

What are the possible solutions?

A few directions emerge from the various studies and reports:

- Recycle CBAM revenue back to developing-country partners, especially for industrial decarbonisation support.

- Mutual Recognition Agreements (MRAs) between Indian verification bodies and EU authorities, so that Indian-certified emissions data is accepted at the EU border.

- Exemptions or transition support for least developed countries.

- A robust, internationally credible Indian carbon price through CCTS, so the carbon money stays inside India.

- Strong Monitoring, Reporting and Verification (MRV) systems at plant level, particularly for MSMEs, so that exporters are not stuck with high default emission values.

- Multilateral climate-trade dialogue to anchor the carbon-trade conversation in WTO and UNFCCC forums, instead of letting it be set unilaterally by Brussels.

Why does this matter?

CBAM is the first serious test of a new idea: that trade policy and climate policy are not separate worlds, and that the carbon content of a product matters as much as its price or quality.

If the Potsdam Institute is right, CBAM could trigger a slow, voluntary spread of carbon pricing across the world's largest economies — climate policy advancing through market logic, not international treaties. That would be a significant development at a time when global climate negotiations have visibly slowed.

If the critics are right, CBAM may end up being a sophisticated form of green protectionism — one that shifts costs onto countries least able to bear them, without delivering the global emission cuts it promises.

For India, the question is no longer whether to engage with carbon pricing. It is how — and on whose terms. The Carbon Credit Trading Scheme, the possible IBAM, the India-EU FTA, the MSME data challenge, and the broader climate-justice argument all converge here.

For UPSC and MPSC aspirants, this is one of those rare topics that cuts across GS Paper 2 (international relations, India and global groupings), GS Paper 3 (environment, climate change, economy, infrastructure), and GS Paper 1 (effects of globalisation on Indian society) — and a question is almost certain to land in one of these papers in the years ahead.